In Part 1, we addressed some of the negative perceptions that exist for cyber insurance, the need for a standalone cyber policy and the difficulty carriers have in pricing premiums. In Part 2, we will explore the premium pricing practices and what to look for in a cyber policy.

How Do Carriers Price Premiums?

According to Founder Shield, underwriters use the following information to price cyber insurance premiums.

- Systems vulnerabilities

- Security training protocols

- Loss history

- Types of data collected and stored

An Advisen whitepaper from 2014 indicates that cyber policy underwriters are also interested in the amount of data a company retains, where data is stored (company server or cloud), and vendor management controls. But, there is no mention of loss history or security training.

In 2016, Jeremiah Grossman, Chief of Security Strategy at SentinelOne said to ITSPmagazine that premiums were based on only two factors – the company’s industry and the number of records it’s stored. In 2017, he added revenue to the equation in an article with Insurance Business.

What’s more interesting is a study done by researchers at RAND. They reviewed policies on file with the insurance commissions in three states (CA, NY, and PA) between 2007 and 2017 to identify how carriers are assessing and pricing cyber risk. The researcher’s analysis revealed five pricing determinants.

1. Outside advice or loss data from industry, academic, and government reports;

2. Competitor’s pricing;

3. The experience and knowledge of the company’s underwriters;

4. Pricing from other insurance lines; and

5. Guesswork.

“From our analysis, the first and most important firm characteristic used to compute insurance premiums was the firm’s asset value (or revenue) base rate, rather than specific technology or governance controls.”

Wait…what?! Cyber insurers don’t care about cyber resilience or best practices?

To be fair, most policies analyzed in the RAND study required self-assessment questionnaires that asked for varying levels of detail related to a company’s security posture. However, questions were mostly focused on data type and volume and not on the security infrastructure.

To address the need for more sophisticated cyber risk assessments, insurers are increasingly turning to technology companies to provide analytics to develop coverage and pricing models. These companies are usually referred to as AppSec or InsurTech providers.

According to The World Insurance Report 2019, over 50% of insurers interviewed indicated partnerships with InsurTech firms or other risk analytics companies. By providing machine learning, aritificial intelligence-based products or advanced analytics, these companies enable underwriters to price risk on limited data.

What to Look For in a Cyber Policy

Before you start to evaluate cyber policies, be sure to select a broker and/or carrier that solely focuses on cyber insurance. Most companies look to buy insurance based on a budget rather than their actual risk exposure. A cyber-experienced broker can guide you to the appropriate coverage specific to your business.

So, what factors are important to consider when reviewing a cyber insurance policy?

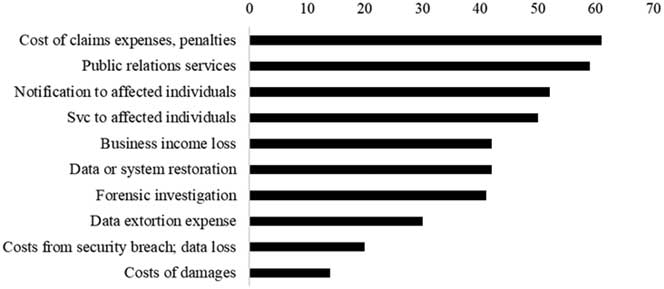

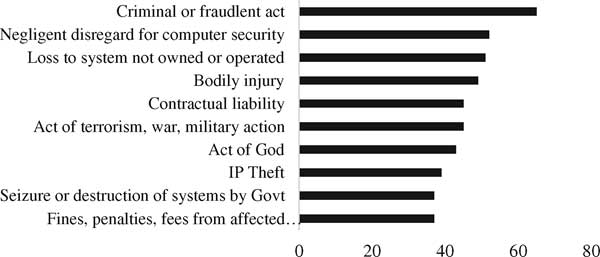

First, all policies list losses that are covered and those that are not. The RAND study compiled lists of the 10 most covered losses and the top 10 exclusions.

Most common covered losses

The ESI SmackDown

The ESI SmackDown